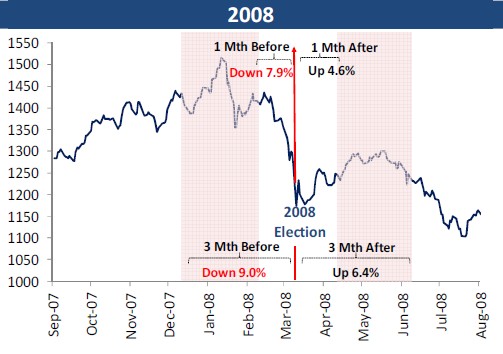

* Note: This is NOT a political post. Instead, we're talking about share market movement based on possible election outcome. Abusive comments are strictly prohibited and will be remove automatically.

Local investors have been staying sideline for months ago. Do you started to feel itchy now? Honestly, this is the feeling of mine as an investor, from being active to passive lately. I can't wait to start investing again in share market. However, we shouldn't simply jump in next Monday, right? Let's see the 3 possible election outcome and how market may react accordingly...

OUTCOME #1: BN retained power

OUTCOME #2: Opposition Alliances won

Many people predicted that market will react negatively to this kind of election outcome. It's not strange. Anyway, once all the worries have settled down, new cabinet was formed, share market will recover. So, an U-shaped rebound is my bet.

OUTCOME #3: Almost 50/50 for Both

This is the worst outcome for share market. A hung parliament does not bode well for the nation. In this situation, very likely, elected assemblyman may jump-ship to another coalition vice versa. So, share market very likely will through months of instability. Dead share market was expected.

Even said so, Bursa Malaysia will definitely still be operating, not as published in one of the advertisement by political party. Hahaha. It's funny to see that kind of advertisement.